Introduction:

The transition to green energy has become a global priority, with many individuals and businesses seeking sustainable solutions to reduce their carbon footprint. Financing green energy projects, however, can be a complex process. Two popular financing options are Commercial Property Assessed Clean Energy (C-PACE) and traditional mortgages. This article aims to provide a comprehensive comparison between these two financing methods, highlighting their advantages and disadvantages.

I. C-PACE Financing:

1. Definition:

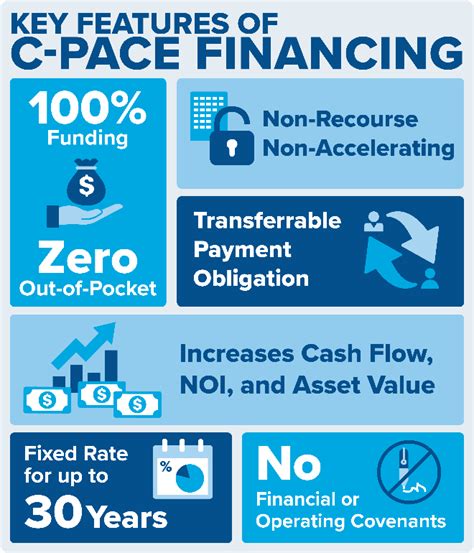

C-PACE is a financing mechanism that allows property owners to fund green energy and energy efficiency improvements through property assessments. The financing is repaid as part of the property tax bill over a set period, typically 10-20 years.

2. Advantages:

a. No upfront costs: C-PACE financing does not require any down payment, making it an attractive option for property owners with limited capital.

b. Long-term financing: C-PACE offers longer repayment terms compared to traditional mortgages, which can help spread the cost of green energy projects over a more extended period.

c. Property value enhancement: Green energy improvements can increase the property’s value, which may offset the cost of financing over time.

d. No effect on personal credit: C-PACE is a commercial financing option, so it does not impact the property owner’s personal credit score.

3. Disadvantages:

a. Availability: C-PACE is not available in all regions, as it depends on local government participation and legislation.

b. Interest rates: While C-PACE offers longer repayment terms, the interest rates may be higher compared to traditional mortgages.

c. Limited use: C-PACE financing is typically limited to commercial properties, which may not be suitable for all green energy projects.

II. Traditional Mortgages:

1. Definition:

A traditional mortgage is a loan used to purchase, refinance, or renovate real estate. The property serves as collateral for the loan, and the borrower repays the loan in fixed monthly installments over a specified period.

2. Advantages:

a. Lower interest rates: Traditional mortgages often have lower interest rates compared to C-PACE financing.

b. Flexibility: Borrowers can use traditional mortgages for various purposes, including purchasing land, constructing buildings, or refinancing existing loans.

c. Availability: Traditional mortgages are widely available and can be used for both residential and commercial properties.

3. Disadvantages:

a. Higher upfront costs: Traditional mortgages usually require a down payment, which can be a barrier for some property owners.

b. Shorter repayment terms: Traditional mortgages typically have shorter repayment periods compared to C-PACE financing, which may result in higher monthly payments.

c. Impact on personal credit: Borrowers’ personal credit scores can be affected by the mortgage process and subsequent payments.

Conclusion:

Both C-PACE and traditional mortgages offer viable financing options for green energy projects. The choice between the two depends on various factors, such as the property type, project scope, and available resources. Property owners should carefully evaluate the advantages and disadvantages of each option to determine the most suitable financing method for their green energy needs.