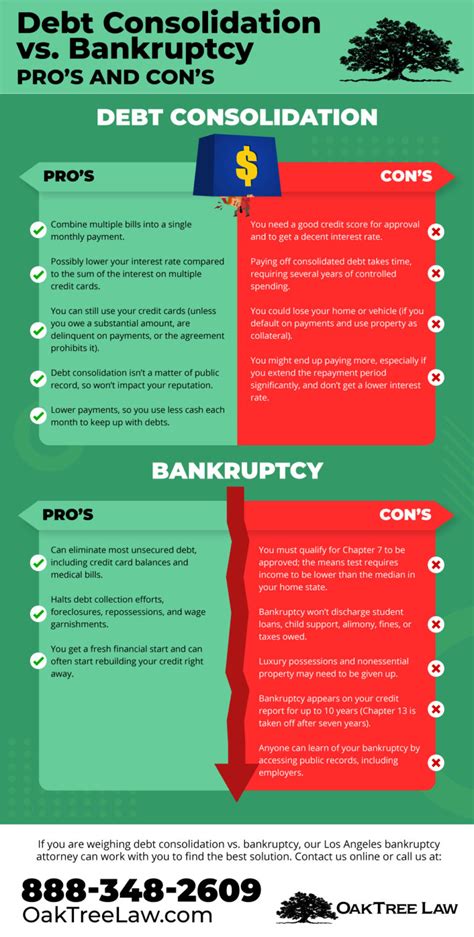

In the modern financial landscape, automated underwriting systems have become a cornerstone of the loan approval process. These systems, powered by complex algorithms, analyze a borrower’s creditworthiness and make decisions with incredible speed and efficiency. However, the increasing reliance on these automated systems has sparked a debate regarding the validity of loan rejection appeals that aim to override these decisions. This article delves into the intricacies of this issue, examining the pros and cons of appealing automated underwriting decisions.

The Role of Automated Underwriting Systems

Automated underwriting systems are designed to streamline the loan approval process by quickly analyzing a borrower’s credit history, income, and other relevant factors. These systems are intended to provide lenders with a fast and accurate assessment of a borrower’s risk profile, allowing them to make informed decisions about loan approvals.

While these systems offer numerous benefits, such as reduced processing times and increased efficiency, they are not without their drawbacks. One of the most significant concerns is the potential for errors or biases in the algorithms that power these systems.

The Importance of Loan Rejection Appeals

Loan rejection appeals provide borrowers with an opportunity to challenge automated underwriting decisions. These appeals can be based on a variety of factors, such as incorrect information in the borrower’s credit report, discrepancies in the loan application, or a belief that the automated decision was incorrect.

Supporters of loan rejection appeals argue that they are essential for ensuring that borrowers are not unfairly denied loans due to errors or biases in the automated underwriting process. By allowing borrowers to present their case, these appeals can help ensure that lending decisions are made on a fair and equitable basis.

The Pros and Cons of Overriding Automated Underwriting Decisions

There are several advantages to allowing loan rejection appeals to override automated underwriting decisions:

1. Fairness: Loan rejection appeals can help ensure that borrowers are not unfairly denied loans due to errors or biases in the automated underwriting process.

2. Transparency: Allowing borrowers to challenge automated decisions can increase transparency in the loan approval process.

3. Improved Accuracy: Reviewing loan applications manually can help identify errors or omissions that could lead to incorrect automated decisions.

However, there are also some disadvantages to consider:

1. Increased Processing Times: Manually reviewing loan applications can be time-consuming, potentially leading to longer processing times for borrowers.

2. Resource Intensive: Manually reviewing loan applications requires additional resources, which could be better allocated to other areas of the lending process.

3. Potential for Bias: Manual reviews may introduce new biases into the lending process, as reviewers may have their own preconceptions or biases.

The Future of Loan Rejection Appeals

As the use of automated underwriting systems continues to grow, the importance of loan rejection appeals will likely become even more significant. To address the challenges and advantages of these appeals, lenders and regulators must work together to develop best practices for handling these cases.

In conclusion, loan rejection appeals can play a crucial role in ensuring that borrowers are not unfairly denied loans due to errors or biases in automated underwriting systems. While there are challenges associated with these appeals, the benefits of maintaining fairness and accuracy in the lending process make them a valuable tool for both borrowers and lenders alike. As the financial industry continues to evolve, it is essential that lenders and regulators find a balance between leveraging the efficiency of automated systems and upholding the integrity of the loan approval process through loan rejection appeals.