Introduction:

Debt charge-offs can be a significant blow to an individual’s financial health, often leaving them with a tarnished credit score and a sense of hopelessness. However, once the 7-year reporting window has passed, there is a glimmer of hope for rebuilding one’s financial standing. This article delves into the strategies and recovery plans that can help individuals overcome the aftermath of a debt charge-off and restore their creditworthiness.

Understanding the 7-Year Reporting Window:

Before delving into recovery plans, it’s essential to understand the 7-year reporting window. According to the Fair Credit Reporting Act (FCRA), a debt charge-off will remain on an individual’s credit report for a maximum of 7 years from the date of the charge-off. This means that once the 7-year mark has passed, the charge-off will no longer impact the individual’s credit score.

Recovery Plan 1: Paying Off Existing Debt

The first step in rebuilding credit after a debt charge-off is to pay off any existing debt. This may seem counterintuitive, but paying off existing debt can help improve your credit score and demonstrate to lenders that you are committed to managing your finances responsibly.

1. Prioritize High-Interest Debt: Focus on paying off high-interest debts first, as they can accumulate interest quickly and make it more challenging to pay off the principal amount.

2. Create a Budget: Develop a realistic budget that allocates funds for paying off debt while still covering essential expenses.

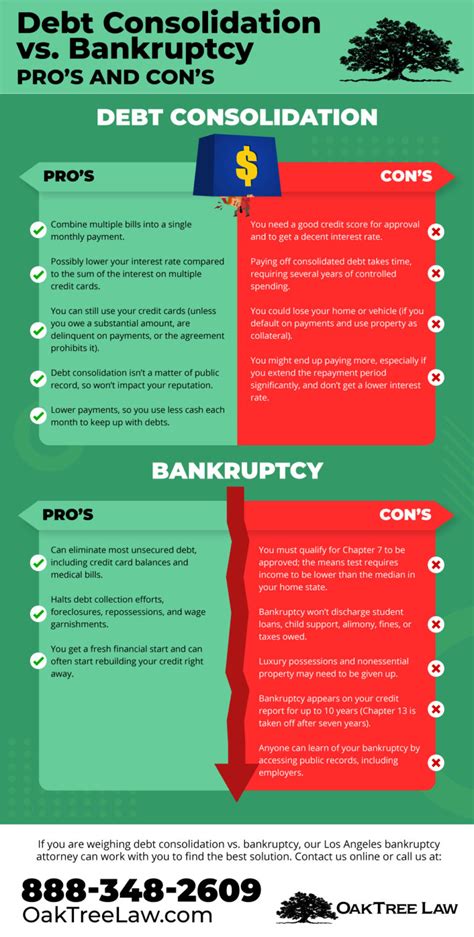

3. Consider Consolidation or Refinancing: If you have multiple debts, consider consolidating them into a single loan with a lower interest rate or refinancing your existing loans to secure a better interest rate.

Recovery Plan 2: Establishing New Credit Lines

After paying off existing debt, the next step is to establish new credit lines to help rebuild your credit score. This can be achieved through the following strategies:

1. Secured Credit Cards: Apply for a secured credit card, which requires a cash deposit as collateral. By making timely payments and keeping the credit utilization low, you can gradually rebuild your credit score.

2. Credit-Builder Loans: These loans are designed to help individuals build credit by making regular payments, which are reported to the credit bureaus.

3. Authorized User: Ask a friend or family member with a good credit history to add you as an authorized user on their credit card. This can help you benefit from their positive credit behavior without taking on any financial responsibility.

Recovery Plan 3: Monitoring Your Credit Score

Monitoring your credit score is crucial in tracking your progress and identifying any potential issues. Here are some tips for monitoring your credit score:

1. Regularly Check Your Credit Reports: Obtain a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year at AnnualCreditReport.com.

2. Use Credit Monitoring Services: Consider using credit monitoring services to receive alerts about changes to your credit report and score.

3. Keep an Eye Out for Identity Theft: Monitor your accounts for any suspicious activity that could indicate identity theft.

Conclusion:

Rebuilding your credit after a debt charge-off can be challenging, but it is not impossible. By following these recovery plans and remaining committed to responsible financial management, you can gradually restore your creditworthiness and pave the way for a brighter financial future. Remember, patience and perseverance are key to overcoming the aftermath of a debt charge-off and rebuilding your credit score.