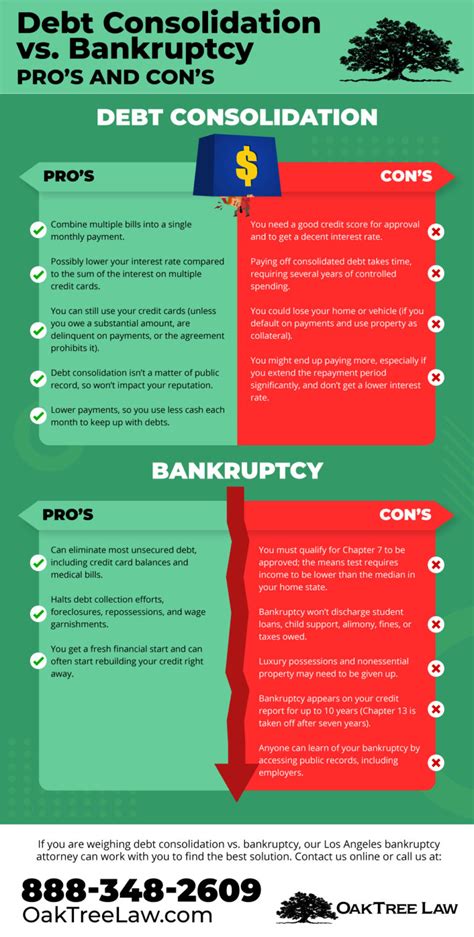

Introduction:

When it comes to loan prepayment, borrowers often find themselves at a crossroads, torn between paying off their loans early to save on interest or facing potential prepayment penalties. This article delves into the comparison between a 2% prepayment fee and the break-even points of interest savings, helping borrowers make informed decisions.

1. Understanding Prepayment Penalties:

Prepayment penalties are fees imposed by lenders when borrowers repay their loans before the agreed-upon maturity date. These penalties are designed to compensate lenders for the lost interest they would have earned if the borrower had continued making regular payments.

2. The 2% Fee:

One common prepayment penalty structure is a flat 2% fee of the outstanding loan balance. This fee is typically charged at the time of prepayment and can vary depending on the lender and the specific loan terms.

3. Interest Savings Break-Even Points:

To determine if prepaying a loan is beneficial, borrowers need to calculate the break-even point, which is the point at which the interest savings from prepayment equal the prepayment penalty. This calculation involves comparing the interest paid on the loan over its remaining term to the penalty fee.

4. Factors Influencing Break-Even Points:

Several factors can influence the break-even points, including:

a. Loan Interest Rate: Higher interest rates can shorten the break-even period.

b. Remaining Loan Term: Shorter loan terms can reduce the break-even point.

c. Prepayment Penalty Structure: Different penalties can affect the break-even point.

5. Example Calculation:

Let’s consider a $100,000 loan with a 5% interest rate and a 10-year term. The monthly payment is $1,013.33. If the borrower decides to prepay the loan, they may face a 2% prepayment penalty.

a. Break-Even Point Calculation:

– Interest Savings: The borrower would save $2,625.60 in interest over the remaining 10 years.

– Prepayment Penalty: The borrower would pay a $2,000 penalty.

– Break-Even Point: The borrower would need to save $2,625.60 in interest to break even, which would take approximately 10 months.

6. Considerations for Borrowers:

When deciding whether to prepay a loan, borrowers should consider the following:

a. Financial Goals: Evaluate if prepayment aligns with your long-term financial objectives.

b. Emergency Fund: Ensure you have an adequate emergency fund before prepaying your loan.

c. Other Opportunities: Consider if there are better investment opportunities than prepaying the loan.

Conclusion:

Loan prepayment penalties, such as the 2% fee, can be a significant factor in determining whether prepaying a loan is beneficial. By calculating the break-even points of interest savings, borrowers can make informed decisions that align with their financial goals and circumstances. Always weigh the pros and cons before deciding to prepay a loan, ensuring you maximize your savings while minimizing potential penalties.