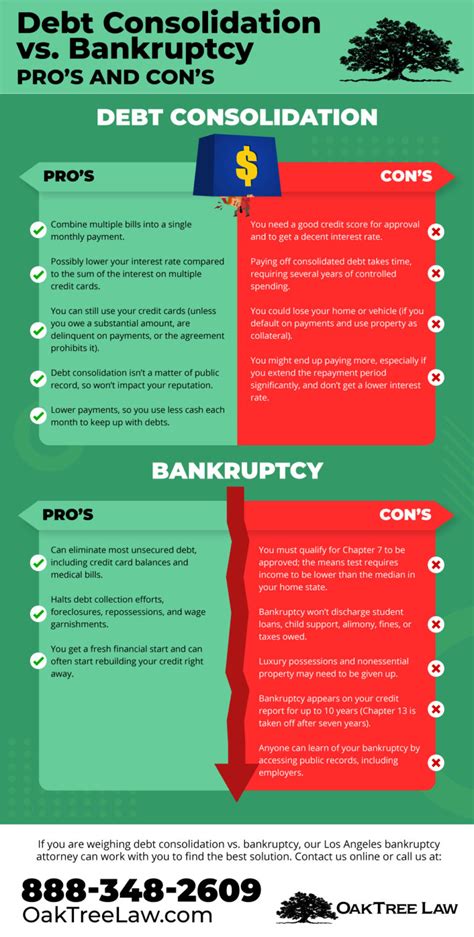

In the digital age, financial institutions are facing an increasing threat of synthetic identity theft, a sophisticated form of fraud that can lead to significant financial losses. This article aims to shed light on the importance of loan fraud alerts and the detection of synthetic identity theft in digital applications.

Synthetic identity theft is a fraudulent practice where cybercriminals create entirely fictional identities by combining real and fake information. These identities are then used to open credit lines, take out loans, or make other financial transactions. As a result, the victims of synthetic identity theft often bear the brunt of financial liabilities and credit damage.

The rapid growth of digital applications in the financial sector has made it easier for cybercriminals to perpetrate this type of fraud. As more individuals turn to online platforms for financial services, the potential for synthetic identity theft detection becomes crucial.

Loan fraud alerts are an essential tool in combating synthetic identity theft. These alerts are triggered when a financial institution detects suspicious activity on a customer’s account. Here are some common signs that may lead to a loan fraud alert:

1. Inconsistencies in personal information: If the details provided by a borrower, such as address, date of birth, or social security number, do not match the records, it could be a red flag for synthetic identity theft.

2. Unusual account activity: Sudden changes in credit limits, multiple inquiries within a short period, or a high credit utilization rate may indicate fraudulent activity.

3. Identity mismatches: When a borrower’s identity does not match the information on their application or existing records, it raises concerns about synthetic identity theft.

To effectively detect synthetic identity theft in digital applications, financial institutions must adopt robust security measures and employ advanced technologies. Here are some strategies to enhance detection capabilities:

1. Real-time monitoring: Continuous monitoring of customer accounts for any suspicious activity can help identify potential synthetic identity theft cases early.

2. Data analytics: By analyzing patterns and trends in customer behavior, financial institutions can detect anomalies that may indicate synthetic identity theft.

3. Artificial intelligence and machine learning: These technologies can identify complex patterns and correlations that may not be visible to human analysts, thereby improving detection rates.

4. Collaboration with credit bureaus: Sharing information with credit bureaus can help identify individuals with multiple identities and flag potential synthetic identity theft cases.

5. Customer education: Educating customers about the risks of synthetic identity theft and the importance of safeguarding their personal information can reduce the likelihood of falling victim to this crime.

In conclusion, loan fraud alerts and the detection of synthetic identity theft in digital applications are crucial for financial institutions to protect their customers and their bottom lines. By implementing robust security measures and leveraging advanced technologies, financial institutions can effectively combat this sophisticated form of fraud and ensure a secure digital financial ecosystem.